World’s top 40 mines drop $156bn in value

It’s well documented that mining companies the world over are struggling to adapt to a climate of depressed commodity prices and sluggish output. But some of the findings in PwC’s latest global mining industry report, Mine 2015, really hit home.Looking collectively at the top 40 mining companies, according to market capitalisation, the report found that market value plummeted 16% by $156 billion in 2014. As a result, the top 40 market capitalisation, now at $791 billion, was at the same level as it was ten years ago.

Changes in top 40 market capitalisation ($ billion) in 2014

Source: Mine2015

“Everyone expected that 2014 would be very tough year when we did the analysis, because of what happened to commodity prices last year,” said Michal Kotze, PwC’s head of mining for Africa.

Confidence was also low, with HSBC Global Mining Index hitting a five-year low in April 2015, at “levels not seen since the last global financial crisis”.

“What is clear is that investors are ringing the changes. They are moving out of investments in the mining indices, (which are being consistently outperformed by other indices),” said Kotze.

Dividend yield was at an all-time high at 5%, but only because companies were trying to maintain paying dividends at a time when their earnings were shrinking.

Net profit excluding impairments fell by 9%, while the return on capital employed (ROCE) fell to 8.4%, the lowest level in the report’s 12-year history. Having been at 9.5% in 2013, this sees the average ROCE continue below the minimum hurdle investment rate of 15-20%.

Only six of the top 40 – Coal India (coal), Norilsk Nickel (nickel), NMDC (iron ore), Randgold (gold), Shandong Gold (gold), and Newcrest (gold) – exceeded this benchmark.

It was also the first time in the report’s history that a South African company was not included in the world’s top 40.

“Anglo American is included, even though it has many South Africa-based subsidiaries. Last year Impala Platinum was there, but it is the first time there are no specifically South African companies in there,” said Kotze.

Five South African companies were included when the first edition of the report was published in 2004.

Miners doing their utmost

Despite difficult circumstances, miners have done their utmost to adapt, with free cash flows turning positive to $24 billion from a $3 billion deficit the previous year. The blow was also softened by an increase in production, currency devaluations, and lower input costs, which boosted margins. The miners also managed to reduce costs, with operating expenses down 5% at $509 billion.

Many companies implemented aggressive cost cutting measures, ranging from staff layoffs, to delaying capital projects, divestiture of non-core assets, and operational improvements.

Impairment charges were down 53% at $27 billion, and this saw the net profit increase 114% to $45 billion in 2014, when impairments were included.

Governments have also intervened in many countries to soften the blow. For example, Indonesia introduced a ban on export of unprocessed mineral ore in an effort to increase domestic processing capacity, while Zambia made some major reductions to taxes applicable to miners.

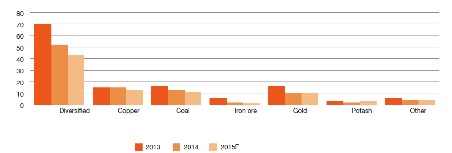

Cutting capex

Top 40 companies reduced capital expenditure across all commodities, with the biggest cuts coming from OECD companies, which slashed capital expenditure by 23%. This was 9% higher than their BRICS counterparts.

The only concern is that this will hamper the ability of the mining sector to be able to produce enough output when the commodity cycle eventually turns around, said PwC assurance partner, Andries Rossouw.

The total asset base of the Top 40 declined by 1% in 2014 compared to an increase of 7% in 2013. Capital expenditures, including non-mining activities, were $103 billion in 2014, versus $129 billion in 2013

Said Rossouw: “It’s a vicious cycle. This is the period when companies should be investing in capacity, but what will eventually happen when the cycle turns, is that companies won’t be able to supply and commodity prices will sky-rocket again. It is just that capital expenditure is one of those discretionary choices that companies elect to cut in difficult times.

Historical and projected annual capital spend by commodity ($billion)

Source: Mine 2015

See the article online here: World’s top 40 mines drop $156bn in value - Mineweb

No comments:

Post a Comment

Commented on MasterMetals